Key Point

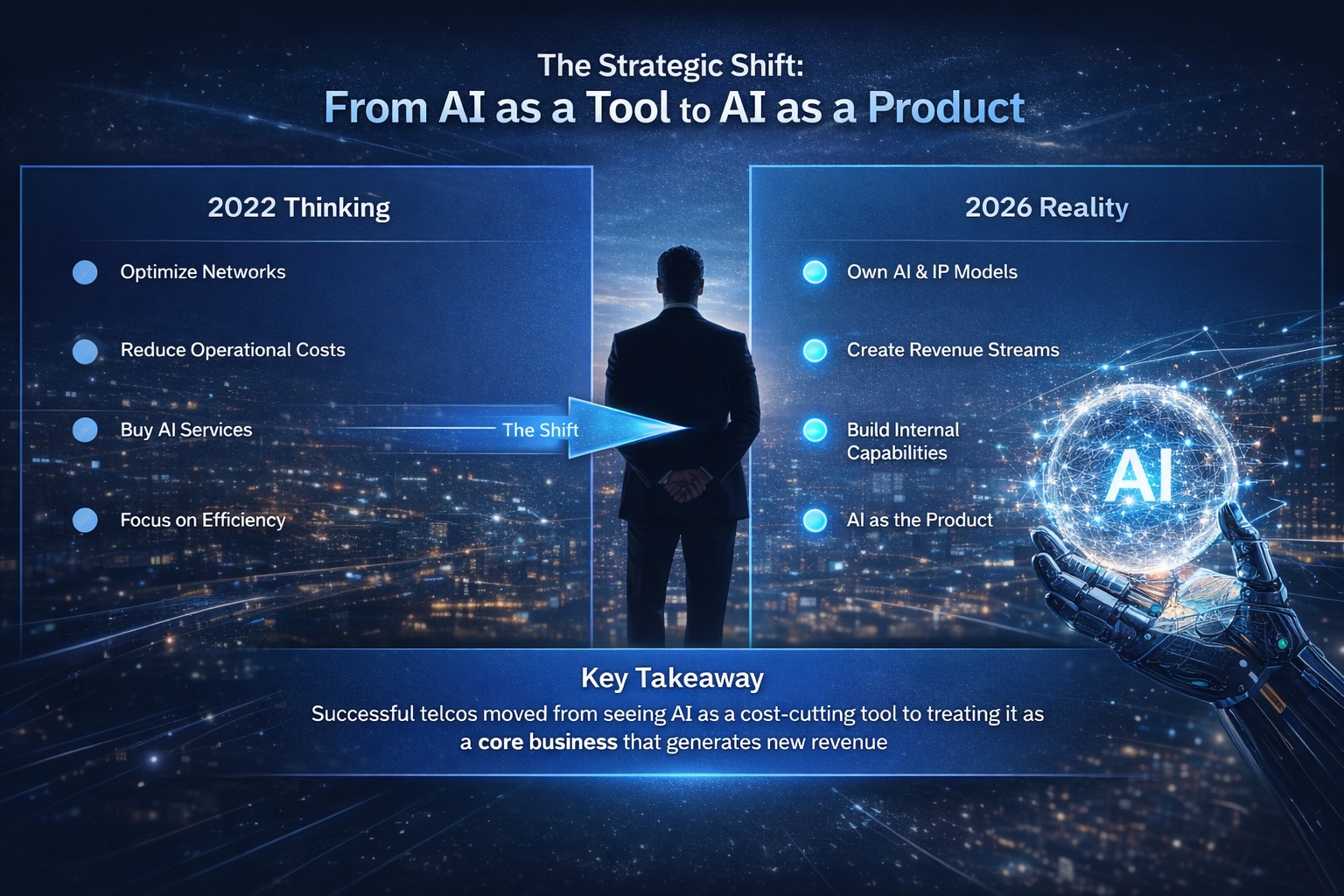

For 2022, we discuss with top level CEOs for telecom clients make dem deploy AI as optimization tool. Years later, we don sabi say we miss road. The real transformation no be about make networks smarter — na about AI to become the product itself. Na wetin I for don tell dem be this.

For early 2022, we don spend months dey analyze network infrastructure, customer data, and operational efficiency gaps. The recommendation strong: deploy predictive maintenance AI, build churn prediction models, optimize network traffic allocation. All of am na sound technical advice. All of am miss the point completely. Four years later, these operators now dey run to catch up with vendors, while competitors wey bet different don completely transform their business models.

For over two decades, I work across telecom, enterprise software, and enterprise infrastructure companies. I witness three major digital transformations: the cloud transition, the shift to software-defined networks, and the move to edge computing. For each one, the pattern na the same: executives wey understand the transformation as technology problem win. Those wey treat am as business model problem win bigger. By 2022, I don pass enough cycles to sabi this. And yet, when e come to AI, I fall inside the same trap wey the industry build. We dey talk AI as tool — something wey dey multiply existing functions. We miss road.

Here na the uncomfortable truth wey most consultants and analysts avoid to talk for 2022: AI been go become product category, no be just optimization layer. And for sector wey mature and margin-constrained like telecom, that shift for be life-or-death matter. The evidence dey visible already, but e easy to miss if you dey focus on quarterly revenue protection instead of five-year business model survival. By mid-2023, when GPT-4 launch and generative AI move from laboratory curiosity to boardroom obsession, the constraint come clear: the organizations wey still dey think AI as 'network optimization' come dey three to four years behind the curve.

Consider the numbers. As McKinsey Q2 2025 AI survey talk, 72% of telecom executives now dey see AI as core business model driver, no be cost optimization tool. But na only 31% of that same group don start to reshape their go-to-market strategies to reflect that reality. Meanwhile, companies like Mistral AI, wey launch for late 2023, capture $950 million for valuation within 18 months — no be because dem better for telecom operations, but because dem position AI as standalone product. For traditional telcos, the lag brutal. Verizon lose $1.2 billion for market share value for Q1 2024 alone as investors rotate comot from telecom as 'legacy infrastructure.' Deutsche Telekom, on the other hand, move faster: by Q4 2024, dem don spin up three separate AI product lines wey target enterprise customers. Their stock recover.

The strategic inflection point wey we miss na this: the margin compression for telecom — the industry core problem for 15 years — been go get solution no by squeezing cost but by creating entirely new revenue streams. And AI, if you position am correct, na the lever. We advise make dem squeeze juice from lemon when we for don advise clients make dem plant apple orchards. One client wey we work with — mid-sized operator with double digit million subscribers — ask for Q3 2022: 'We suppose build internal AI lab or buy AI services?' We for recommend buying. The logic na economical: faster time-to-value, lower capital risk. Wetin we for don talk na this: 'Build. You need to own the IP, the talent, and the business model optionality. For 18 months, AI no go be cost center — e go be your highest-margin business unit.'

By 2024, the same operator don make different choice. Dem hire 120 ML engineers, partner with local universities, and build three AI-powered customer service solutions. Today, those products dey account for 12% of their B2B revenue — $180 million annual run rate on wetin dem suppose be 'defensive' investment. That no be anomaly. Orange, Telefónica, and BT Group follow similar patterns. The ones wey listen to legacy consulting advice — the 'make we optimize wetin we get' school of thought — now dey for 2026 dey discuss defensive M&A or infrastructure consolidation.

The deeper issue na say the telecom industry don spend so long dey think about AI through the lens of operations that e miss the market shift wey dey happen for open eye. From 2021 through 2023, enterprise customers dey desperate for specialized AI models: industry-specific language models, domain experts wey dem embed inside SaaS platforms, agentic AI wey fit handle end-to-end business processes. Telecom get the assets — massive datasets, regulatory expertise, customer relationships — to dominate three of those categories. Instead, the industry dey debate whether Hugging Face or OpenAI na the better partner. Na so you take measure the size of the strategic misread.

Here na wetin change the thinking. For 2022, our mental model na: 'AI dey help you run your existing business better.' By late 2023, that model don old. The new model na: 'AI na new business unit wey need im own P&L, im own hiring profile, im own go-to-market, and im own board-level oversight.' For telecom operators, that mean say dem go make choice by early 2024: We go invest to become AI company wey happen to operate network, or we go remain network operator wey dey play small small with AI? The ones wey choose the former — and choose am with mind — don create entirely new competitive positions.

Take Vodafone as example. For Q4 2023, dem launch Vodafone AI — separate business unit with im own branding, im own product roadmap, and $500 million committed investment over three years. E look like risk at the time. Some analysts call am distraction. By Q3 2025, Vodafone AI don sign contracts with 140+ enterprise customers, at average contract value of $2.1 million yearly. The unit now dey on track to be cash-flow positive by Q2 2026. That no be optimization. That na transformation. And e happen because person inside Vodafone ask the right question: 'Wetin if AI no be feature of our core business — wetin if e be our next core business?'

The generational shift wey dey happen right now na the move from 'narrow' AI (dey optimize specific functions) to agentic AI (dey make autonomous decisions within defined domains). For telcos, this na $45 billion opportunity by 2028, as Forrester latest analysis talk. But na only if dem don already make the mental shift wey we describe. If you still dey for 2022-thinking, this transition go look like confusion. If you dey for 2026-thinking, e be runway. The operators wey invest for AI talent pools, data infrastructure, and regulatory expertise between 2023 and 2025 now get three-year head start on everybody else. The ones wey no do dey run hiring freezes now and dey sell off infrastructure assets.

We for don get this for 2022: Stop to think about where AI dey optimize your network. Start to think about wetin new markets AI dey let you serve wey you no fit serve before. The answer, for most telecom operators, involve selling AI-driven services to enterprises for healthcare, financial services, and manufacturing. E involve building proprietary models wey dem train on telecom unique data. E involve competing with OpenAI and Anthropic, no be to partner with dem. That no be comfortable message for most CIOs for 2022. E for don mean bigger budgets, faster hiring, longer payback periods. E for don mean to treat AI as business transformation, no be cost reduction initiative. Most telcos choose comfort. Four years later, dem dey pay for am.

The hard truth na say transformation advice na only valuable if e contrarian enough to move the needle and grounded enough to execute. For 2022, we fail on the first dimension. We too near consensus, too focus on de-risking, too comfortable with incremental thinking. Clients no need expensive consultant to tell dem wetin their IT vendors dey already sell. Dem need person to tell dem say the industry been go realign around entirely different economics. That person for don be me. E no be.

If you dey run telecom operator today, here na the three questions to ask yourself for 2026: First, we get standalone AI business unit with im own P&L and board accountability? Second, we dey hire more ML engineers and product managers pass network engineers? Third, our biggest revenue deals now dey driven by AI capabilities instead of connectivity and infrastructure? If you answer 'no' to all three, you dey for the operational tail of this transformation. You still get time to catch up, but the window dey close. The ones wey move with mind between 2023 and 2025 don build unfair advantages. The ones wey no do dey about to find out wetin real disruption be.

The real lesson no be about getting AI predictions right. Na about recognizing when an industry central question don shift. For 2022, telecom question na 'How we go stay relevant?' By 2024, the question don become 'Wetin new market we go own with AI?' By 2026, e don become 'We fit compete with pure-play AI companies?' Four years na long time for technology. Make sure say you dey answer the question wey the industry dey ask today, no be the one wey e dey ask three years ago. Na that insight we for don offer my clients. Na that insight we dey offer now.

For more articles visit our website: telcotank.com

Hakan Dulge

Founder & Managing Director, Telcotank. 20+ years for telecom transformation, AI strategy, and digital infrastructure advisory.